Top 4 Reasons Why TSP Lifecycle Funds May Miss the Target

- Tyler Weerden

- Jun 5, 2024

- 8 min read

Updated: Jul 12, 2025

What is a Lifecycle Fund

Lifecycle Fund, Target Date Fund, LifeStrategy Fund, Target Retirement Date Fund. Regardless of the branding, these funds are all constructed around the same concept. The further away you are from a specific date, the more aggressive your investment portfolio can be, generally meaning more stocks and less bonds. As you get closer to that target date, the asset allocation shifts and becomes more conservative (fewer stocks, more bonds).

The Thrift Savings Plan (TSP) Lifecycle Funds consist of a diversified mix of the individual core funds. U.S. stocks (C & S Funds), international stocks (I Fund), and bonds (F & G Funds). Note: the TSP G Fund earns bond-like returns but does not have the same risk as a bond fund, since the U.S. government guarantees principal protection. As an example of Lifecycle Fund asset allocation, as of May 2024, the L 2025 Fund has a target bond allocation of 67.31% (G & F Funds) while the L 2065 Fund has a target bond allocation of just 1% (G & F Funds).

TSP rebalances the L Funds daily and the overall target allocation of the fund is adjusted every quarter, slowing becoming more conservative over time. Once the L Fund reaches the target date, it ceases to exist and your money is moved into the L Income Fund. As of February 2024, there were over 7 million TSP accounts with over $877 billion in assets. Of these accounts, 38% (2.67 million) were 100% invested in L Funds.

What’s to Love?

Lifecycle Funds are low-cost, diversified, and simple. There’s no debating that one of the primary risks to investors is their behavior. Those implementing a “set it and forget it” approach tend to avoid market timing, stock picking, and emotional financial behavior. Also, with a single L Fund, you don’t have to deal with transfers to or from multiple funds when you decide to rebalance.

Since 2015, L Funds have been the default investment for new employees who are enrolled in the TSP through automatic enrollment. Prior to having L Funds as the default investment, new employees’ contributions were made in the G Fund. Hopefully we’ve seen the last of the days where federal employees unknowingly parked their retirement savings in the risk-free, low volatility, lower returning G Fund for a decade simply due to automatic enrollment. This isn’t a knock on the G Fund, which certainly serves a purpose for many federal employees. However, for the vast majority of new hires, 100% of their contributions should not be sitting in the G Fund.

Now, for the four potential downfalls.

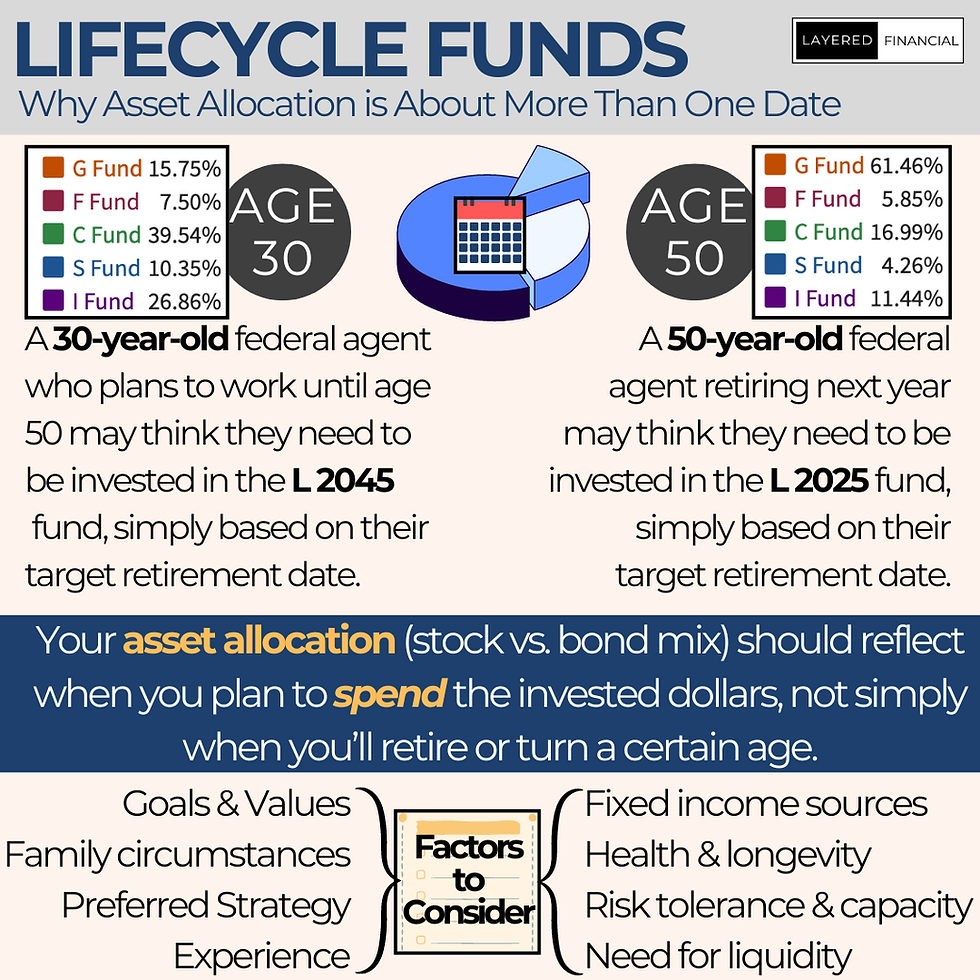

#1 – Time Horizon

“I’m going to retire next year” means something completely different than, “I’m going to pull money from my TSP next year.” Investors would be better suited if they stopped thinking of time horizon in terms of their age, or their retirement date. Instead, investors need to consider the “lifecycle” or “expiration date” of their dollars.

The dollars set aside for next month’s rent, your child’s education in 10-years, and your retirement in 30-years each have very different time horizons. If you have dollars that will “expire” / be used next month for necessities, you don’t want them invested in something that could decline by 30% by next month (from 2/19/20 - 3/23/20, the S&P 500 declined over 33%). On the other hand, if your dollars aren’t going to be used for 30-years, you don’t want them sitting in cash being eroded by inflation. The idea that your time horizon and asset allocation are simply based on your age or a specific date is why we see federal retirees move all of their money to the G Fund, even when they don’t plan on withdrawing money for decades. This can be a costly mistake.

#2 – Too Conservative?

Another potential flaw with target date style funds is that they tend to shift overly conservative (heavier allocation towards bonds) too soon, especially for federal employees who can retire much earlier than traditional retirement age.

Someone retiring in 20-years may think the L 2045 fund is the place for them. As of 7/12/25, The L 2045 Fund has 23.25% allocated to the G and F Funds. A FERS Special Provision Employee hired today at age 21 could technically retire at age 46 and live until age 96. Should they really have 23.25% in bonds today?

Let’s think of a federal employee retiring next year who therefore thinks they need to be in the L 2025 Fund, which has a 67% bond allocation. What if they’re a healthy 55-year-old with other income sources that cover their expenses, and two parents still living in their 90’s? A 67% bond allocation may not provide the return they need in order to meet their long-term goals.

Investors need a healthy portion of their dollars invested in assets that will hopefully beat inflation, or at least keep pace with it. Historically, stocks have been a sound hedge against inflation. Of course, past performance is no guarantee of future returns.

Federal employees need to remember that the G and F Funds represent fixed income. Most federal employees will be retiring with multiple fixed income sources, specifically their federal pension (“annuity”), possibly a Retiree Annuity Supplement, and Social Security. This isn’t even considering other income sources such as rental income, VA disability, a working spouse, or “fun money” from post-retirement employment.

Why do these funds tend to skew more conservative even for young investors? Some say it’s a tactic by the fund company to keep people invested in the fund by reducing volatility through bonds. Moving away from the cynical fee theory, the conservative nature of these funds may simply be a legislative effect.

The Pension Protection Act of 2006 included regulatory provisions for automatic enrollment, and Qualified Default Investment Alternatives (QDIA) for new employees. The regulation notes that QDIAs, “must be diversified so as to minimize the risk of large losses.” 29 CFR § 2550.404c-5 details that a QDIA can be an investment product that provides, “long-term appreciation and capital preservation through a mix of equity and fixed income exposures based on the participant's age, target retirement date (such as normal retirement age under the plan) or life expectancy.”

It’s clear that the government wants employees to be automatically enrolled in an investment less cautious than 100% bonds, but also doesn’t want them invested in something that may cause them to emotionally jump out of the market due to a large downturn.

Additionally, after the Global Financial Crisis, the Securities & Exchange Commission and the Department of Labor held a joint hearing in June 2009 centered around the use of target date funds. SEC Chairman Mary Schapiro noted that, “the average loss in 2008 among 31 funds with a 2010 target date was almost 25 percent. Returns of 2010 target date funds in 2008 range from -3.6% to -41%.” This Congressional spotlight may have resulted in target date fund providers to shift more conservative to avoid large losses should another financial crisis occur.

#3 – Overlap

Lifecycle Funds may cause some unintentional overlap and higher concentration towards stocks or bonds than desired. These funds are designed to be a single holding, representing a total asset allocation mix. Instead, some TSP participants are invested in a Lifecycle Fund plus additional individual TSP funds, or multiple Lifecycle Funds with different target dates.

2.87 million TSP participants accounts are invested entirely in L Funds. As of 5/31/25, 1.09 million TSP participants have chosen to use a mix of L Funds and underlying funds. Using various Lifecycle Funds at the same time, or investing in a Lifecycle Fund combined with individual core funds (C,S,I,F,G) is where we could see some overlap and/or unintended asset allocation.

Let’s look at someone who retires this year, currently 100% invested in the L 2025 fund. The retiree was told by colleagues that they should move half of their money to the G Fund for safety and to weather stock market declines in retirement. Unfortunately, they don’t realize there’s already a large allocation to the G Fund within the L 2025 Fund. If this retiree moved half of their TSP to the G Fund and kept the other half in the L 2025 Fund, they would have 81% in the G Fund. Whereas before, if they kept all of their money in just the L 2025 Fund, they would have 61% in the G Fund.

Now, take someone who invests in the L 2045 fund and decides they want more exposure to the C Fund. If they don’t truly understand how the L Funds work, they may start splitting their contributions and put money in both the L 2045 Fund and the C Fund. Now, when they go to rebalance, they have to calculate their total C Fund exposure across both the L 2045 Fund and the C Fund. A more optimal solution to maintain a single fund holding would have been to simply switch from the L 2045 Fund to the L 2055 Fund, which allocates more to the C Fund.

#4 – Fees

While the L Fund expense ratios are very inexpensive compared to actively managed funds, every dollar paid in fees matters. Lifecycle Funds and target date funds offered by non-TSP custodians tend to have slightly higher fees than a simple passive index fund. The higher fees are caused by more required maintenance such as daily rebalancing and quarterly asset allocation adjustments. Higher fees erode your total return and result in fewer dollars compounding.

Bottom Line

Lifecycle Funds are not bad, especially when it comes to the benefits of being the default investment for auto-enrollment versus the prior G Fund investment default. Lifecycle Fund investors need to be cognizant of higher fees, unintentional overlap/concentration, improper time horizon, and shifting too conservative too soon.

To conduct a proper asset allocation determination, investors need to not just consider their age and retirement date, but also family dynamics, goals and values, health status, outside investment accounts, income sources, expenses, assets, debts, and legacy wishes. Once an asset allocation is decided, investors can create their own low-cost, diversified, “target date” portfolio by simply adjusting their TSP individual fund holdings as their age, risk profile, and unique life circumstances change.

About the Author

Tyler Weerden is a fee-only financial planner and the owner of Layered Financial, a Registered Investment Advisory firm based in Arlington, Virginia. In addition to being a financial planner, Tyler is a full-time federal agent. He holds a Bachelor of Science degree, a Master of Science degree, passed the Series 65 exam, and is a Certified Fraud Examiner (CFE). Tyler is the sole Investment Adviser Representative at Layered Financial.

Prior to becoming a federal agent, Tyler served as a state trooper, local police officer, and was a member of the U.S. Army National Guard. He has served in both domestic and overseas Foreign Service assignments. Tyler has experience with local, state, and federal pension systems, 457(b) Deferred Compensation, the federal Thrift Savings Plan (TSP), Individual Retirement Accounts (IRAs), Health Savings Accounts (HSAs), and various investment options to include rental real estate.

Disclaimer

Layered Financial is a Registered Investment Adviser registered with the Commonwealth of Virginia and State of Texas. Registration does not imply a certain level of skill or training. The views and opinions expressed are as of the date of publication and are subject to change. The content of this publication is for informational or educational purposes only. This content is not intended as individualized investment advice, or as tax, accounting, or legal advice. Nothing in this article should be seen as a recommendation or advertisement. Layered Financial and its Investment Advisor Representatives have no third-party affiliations and do not receive any commissions, fees, direct compensation, indirect compensation, or any benefit from any outside individuals or companies. Although we gather information from sources that we deem to be reliable, we cannot guarantee the accuracy, timeliness, or completeness of any information prepared by any unaffiliated third-party. When specific investments, types of investments, products, or companies are mentioned, such mention is not intended to be a recommendation or endorsement to buy or sell the specific investment, solicit the business, or use that product. The author of this publication may hold positions in investments or types of investments mentioned in articles. This information should not be relied upon as the sole factor in an investment-making decision. Readers are encouraged to consult with professional financial, accounting, tax, or legal advisers to address their specific needs and circumstances.

© 2024 Tyler Weerden. All rights reserved. This article may not be reproduced without express written consent from Tyler Weerden.